In recent years, critics of the Rashtriya Swayamsevak Sangh (RSS)—India’s largest volunteer-based socio-cultural organization—have often questioned why it is not registered as a non-governmental organization (NGO). Such criticisms frequently imply that the RSS operates in a legal gray area or lacks transparency regarding its finances.

However, a review of India’s judicial and tax records tells a different story. Over several decades, Indian courts and tax authorities have repeatedly examined the legal status and financial structure of the RSS. Their rulings have established that the organization’s legality does not depend on NGO registration and that its principal funding mechanism, known as Guru Dakshina, has been subjected to judicial scrutiny.

Understanding the RSS Structure

The RSS, founded in 1925, functions primarily through a nationwide network of daily local gatherings known as shakhas, where volunteers meet for physical activities, community engagement, and ideological discussions.

Many public-facing activities associated with the broader RSS ecosystem are conducted through independent entities that are formally registered as charitable trusts, societies, or NGOs. The RSS itself, however, operates as a voluntary membership organization.

Its internal activities are financed largely through Guru Dakshina, an annual voluntary contribution made by members, known as swayamsevaks.

Historical Scrutiny of the RSS

The RSS has been banned three times in independent India’s history—in 1948, during the Emergency in 1975, and in 1992. On each occasion, the ban was imposed by governments led by the Indian National Congress.

Given the political significance of these bans, government authorities extensively examined the organization’s structure and operations. In addition, the RSS has been involved in numerous legal proceedings over the decades.

Despite this scrutiny, neither the Indian government nor the judiciary has ever questioned the organization’s basic legal existence or required it to register as an NGO. The only major structural requirement imposed by the government came in 1948–49, when authorities asked the RSS to adopt a written constitution, which it subsequently did.

The Constitutional Framework

India’s Constitution guarantees citizens the right to form associations under Article 19(1)(c). Registration as an NGO is not a prerequisite for every voluntary organization operating within the country.

Under Indian tax law, voluntary associations may exist in different legal forms. Two relevant categories are:

- Association of Persons (AOP), a category often associated with formally organized groups; and

- Body of Individuals (BOI), a recognized legal category that does not necessarily require registration as an NGO.

Indian tax authorities and tribunals have long treated the RSS as a legitimate collective entity within this legal framework.

The Landmark Tax Case

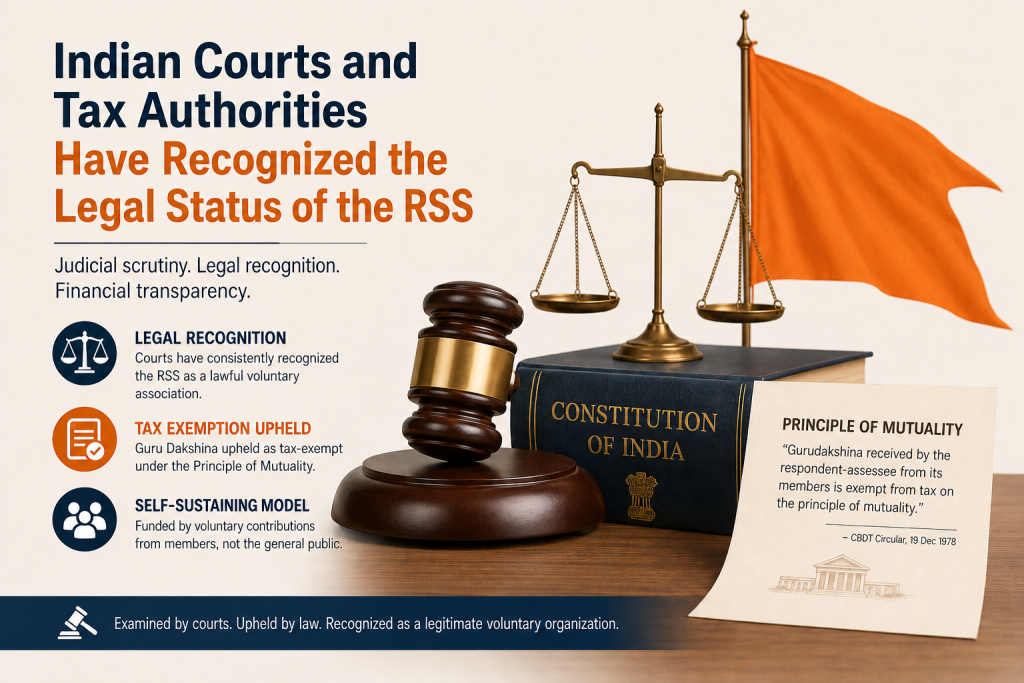

The most significant judicial examination of the RSS’s financial model came in the case of Commissioner of Income Tax v. Rashtriya Swayamsevak Sangh (1994).

The dispute concerned whether Guru Dakshina contributions collected by the RSS during the assessment years 1967–68 to 1975–76 should be treated as taxable income.

The Income Tax Department argued that because individual contributors were not recorded in a manner comparable to commercial accounting systems, the contributions should be taxed. The RSS maintained that the funds represented voluntary contributions from members and therefore qualified for tax exemption.

The matter progressed through India’s Income Tax Appellate Tribunals before reaching the Patna High Court.

The Principle of Mutuality

A key factor in the court’s decision was a circular issued by India’s Central Board of Direct Taxes (CBDT) on December 19, 1978. The circular stated:

“Gurudakshina received by the respondent-assessee from its members is exempt from tax on the principle of mutuality.”

The court was asked to determine:

- Whether the principle of mutuality applied to the RSS; and

- Whether contributions received from members could legitimately be classified as Guru Dakshina and therefore be exempt from taxation.

The Patna High Court answered both questions in favor of the RSS.

In its ruling, the court held that the principle of mutuality did apply and that contributions received from members could be treated as Guru Dakshina and exempted from income tax.

What Is the Principle of Mutuality?

The principle of mutuality is a well-established doctrine in common-law tax jurisprudence. It rests on a simple proposition: individuals who contribute to a common pool for their own collective, non-commercial benefit cannot be treated as generating taxable profits from themselves.

The doctrine is commonly applied to clubs, associations, and membership-based organizations where contributors and beneficiaries are effectively the same group.

By recognizing the RSS under this principle, both the CBDT and the judiciary acknowledged that the organization operates as a self-financed membership body rather than as a commercial enterprise generating taxable income from the public.

What the Legal Record Shows

The legal significance of these rulings extends beyond taxation. They demonstrate that Indian authorities have repeatedly recognized the RSS as a lawful and identifiable collective entity operating within the framework of Indian law.

The courts did not treat the RSS as an unregistered or extra-legal body. Rather, they examined its organizational structure, assessed its funding model, and applied established legal doctrines to determine its tax obligations.

As a result, the historical record suggests that the RSS’s legal standing in India has never depended on obtaining NGO registration. Instead, Indian courts and tax authorities have consistently treated it as a legally recognized voluntary association whose financial practices are subject to established legal oversight.